Most of the investing world gets a bit weird around the Federal Open Market Committee (FOMC) meetings, which is where the nation’s central bank announces its latest interest rate policy. The announcement concerns the overnight borrowing rate for banks that need short-term financing if they run (temporarily) short on liquidity. The idea is that if the Fed (short for Federal Reserve) raises or lowers this rate, then interest rates throughout the economy will shift up or down accordingly, raising or lowering the cost of financing for America’s corporations (and consumer mortgage rates, money market rates, etc.) and potentially leading to recession (and lower stock prices) or economic prosperity (and higher stock prices).

If you believe any of that, then the FOMC meeting on December 13th delivered some good news. The committee’s economists and bankers voted unanimously to keep the benchmark overnight borrowing rate somewhere between 5.25% and 5.5%. They also projected (no guarantees, of course) that there would be three rate cuts in 2024, which observers assume will be 0.25% each.

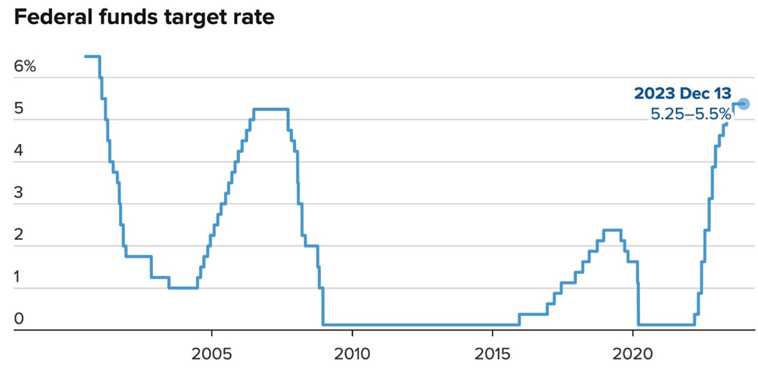

It’s worth noting that the Fed has initiated 11 rate hikes in the last two and a half years (see chart), taking the Fed Funds rate to its highest level in more than two decades. If you follow the logic that drives people to obsess over FOMC announcements, then you might think that this was a sure recipe for economic disaster and pundits have been predicting for much of these past two and a half years that the U.S. was destined for a painful recession. However, the most recent economic reports have shown extraordinary growth in the U.S. economy (5.2% annualized in the 3rd quarter) and the U.S. investment markets have recently topped their all-time highs.

Source: Board of Governors of the Federal Reserve System (US)

Source: Board of Governors of the Federal Reserve System (US)

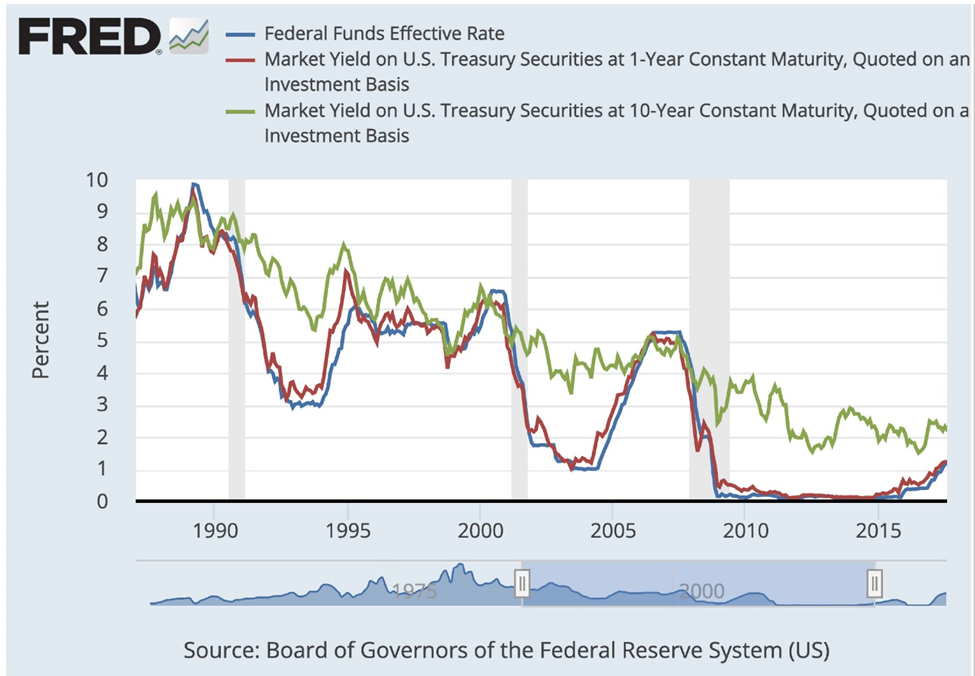

We might also wonder if it’s true that changes in the Fed Funds rate has a direct impact on interest rates. A 2017 study by the Federal Reserve Bank of St. Louis, a particularly astute group of Fed economists, in our opinion, shows that short-term (1-year) Treasury rates tend to follow the Fed Funds rate pretty closely, but when you move out to ten-year maturities, there is very little correlation (see chart below). Long-term rates—whether it be government securities, corporate bonds, or municipal obligations—are driven by market forces, by supply and demand, and buyer expectations around inflation and the economy, as a whole. Corporations and consumers can potentially lock in these longer-term rates or yields pretty much independently of whatever is announced at the FOMC meeting.

Wait a minute! Does that mean we should ignore the Fed’s periodic announcements? The answer for the average investor is probably yes. The same is true about pundits, soothsayers, and anybody else who is contributing to the noise around short-term investing. We believe the only way to make money in the investment markets is to tune out the chatter and let all the workers who wake up every morning and go to work at their various jobs create value in the stocks you and your clients own, day by day, over the long haul. Everything else—even pronouncements by the mighty Fed—is irrelevant white noise and not worth watching in our opinion.

Sources:

https://www.cnbc.com/2023/12/13/fed-interest-rate-decision-december-2023.html

Apella Capital, LLC (“Apella”), DBA Apella Wealth is an investment advisory firm registered with the Securities and Exchange Commission. The firm only transacts business in states where it is properly registered or excluded or exempt from registration requirements. Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Apella Wealth provides this communication as a matter of general information. Any data or statistics quoted are from sources believed to be reliable but cannot be guaranteed or warranted. Apella Wealth does not provide tax or legal advice and nothing either stated or implied here should be inferred as providing such advice.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.